Is Debt Consolidation a Good Idea?

01/05/2024

By: Lindsey Fredericks

Debt can be a major source of stress for many people, especially if you’re dealing with debts in different areas of your life. The average Pennsylvanian has over $80,000 of outstanding debt, so if you’re one, you may want to think about how to pay down debt in 2024 using debt consolidation.

Debt consolidation may help you to lower the overall financial stress you’re currently feeling, but if this isn’t something you’ve done before, you may not know where to start. Questions like “is debt consolidation a good idea?” might be coming up, so we’re here to walk you through exactly what this process can look like.

What is Debt Consolidation?

When you consolidate debt, you take multiple existing debts and combine them into a single loan. This loan is then used to pay off your existing debts, which means you’re only paying one loan with a single interest rate instead of multiple loans each month.

This is a great approach when you’re thinking about how to lower debt in your life, as you can avoid higher interest rates by consolidating everything into a single, lower rate loan. It’s not only helpful for your wallet, but also for keeping organized—one loan is much easier to remember to pay than multiple bills at the same time.

What Types of Debt Should You Consolidate?

Not all debt is bad. When you buy a house and take out a mortgage, it’s a debt that can be beneficial for many years. You’re getting on the property ladder and you can write off the mortgage interest you’ve paid on your taxes each year. You’re also putting a roof over your head without the stress of rent increases or landlords asking you to move.

Student loans can also be a good debt if you’re investing in your career. Some occupations require you to have a degree, or even advanced degrees, to continue your upward progression. While these may seem expensive at first, your future salary will likely take care of these loans and make it worth the cost.

When you’re thinking about a debt consolidation loan, you want to start with the bad debts that don’t benefit you. These could be credit card debts, high interest rate personal loans, or other student loans you might have.

The loans with variable rates can end up costing you hundreds, if not thousands, of dollars in extra money when you’re carrying a balance. Make sure these loans are paid off as quickly as possible.

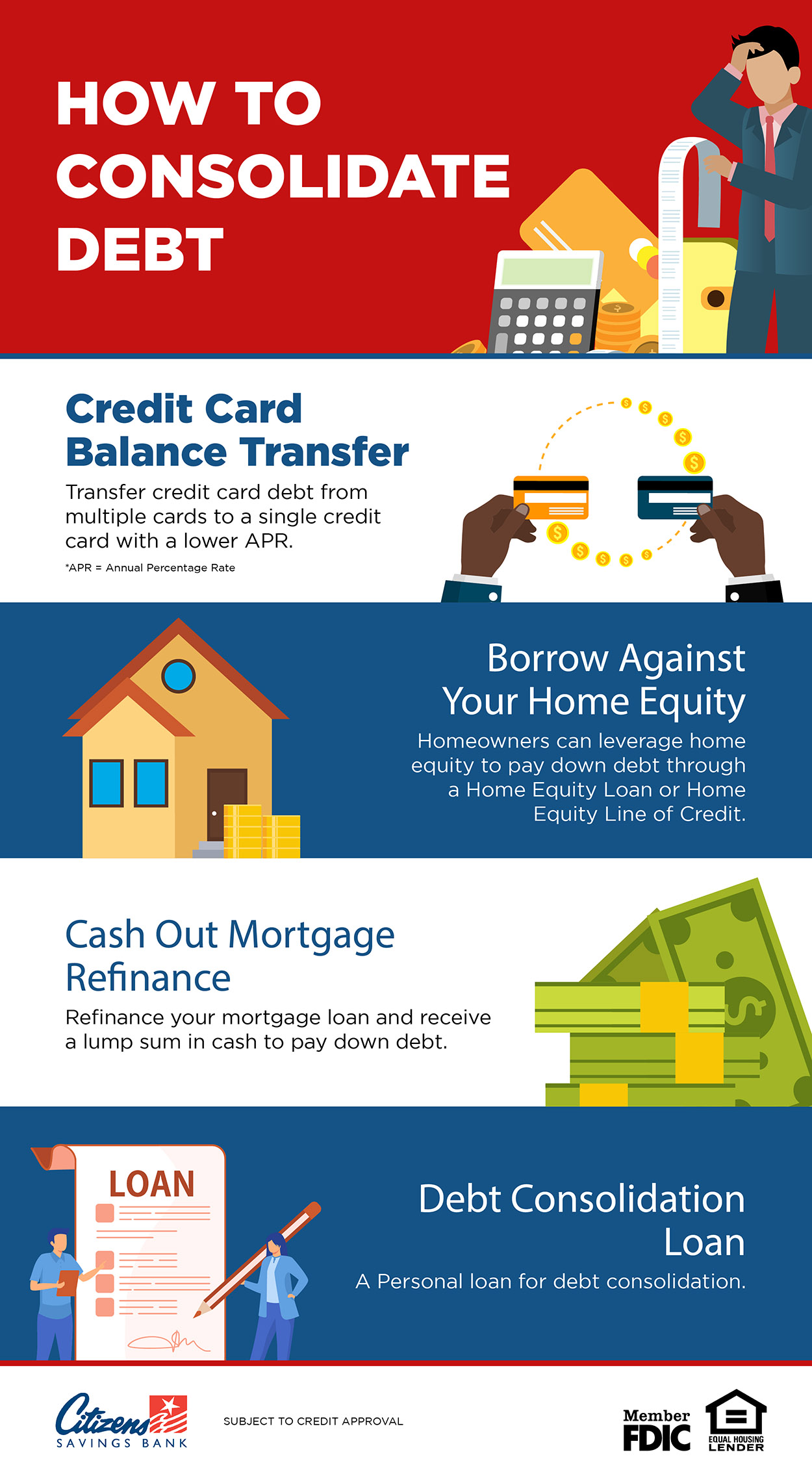

How to Consolidate Debt

Credit Card Balance Transfer

If most of your debt is currently on credit cards, opening a new credit card with a low APR for balance transfers can be a good option. Look at the terms carefully, though. These APRs are typically for a limited, introductory time only.

But if you can pay off the balance before that time expires, you could benefit from lower interest rates than those of your current credit cards.

Borrow Against Your Home Equity

If you’re a homeowner, you can borrow against the equity you’ve built in your home. Home equity is the difference in the amount of money you owe on your mortgage and the current value of your property.

With a home equity loan, you can borrow from 5 to 15 years. For example, if you have a $400,000 mortgage but your home is now worth $500,000, you could borrow up to 80-85% of the $100,000 difference.

Home equity lines of credit also work in a similar way, allowing you to borrow against the value you’ve built up in your home. However, these work much like a credit card, but without a physical card in your hand.

With a home equity loan, you’ll be taking a fixed amount. But with a home equity line of credit, you can be approved up to a set limit, but borrow as much or as little as needed under that limit. Once you’ve repaid it, you can reuse that line of credit again until the loan’s expiration date.

Home equity loans and HELOCs often have lower interest rates than personal loans for debt consolidation or other consolidation options, so it can be worth doing if you know you can pay the amount borrowed back. Failure to pay back your loan can have severe consequences, like home foreclosure, so it’s important to consider all of your options before choosing this.

Cash Out Mortgage Refinance

Another home lending option is to refinance your mortgage with a cash out. This means replacing your existing mortgage with a new one, but taking a higher loan out than what you need for your home.

The cash difference between your loan amount and what you need to pay off your existing mortgage is then cash you can use to consolidate and pay off other debts.

While a lump sum payment like this can be useful, it’s important to remember that a higher mortgage amount will increase your monthly mortgage payments, unless you’ve moved from a very high interest loan to a low interest loan. This is a critical factor to consider when budgeting for this type of debt consolidation.

Debt Consolidation Loan

You can also take out personal loans for debt consolidation. Personal loans can be used for almost anything, so this can be a useful option to consider if you don’t want to risk your home or other assets.

These loans can be helpful if you’re looking to consolidate debt so that you only have one loan to pay off. You should look at both secured and unsecured loans before making a final decision.

Secure loans allow you to use your savings as collateral, which often gives you lower interest rates. Unsecured loans don’t require any kind of collateral, but may have higher interest rates as a result. As a customer of Citizens Savings Bank, both certificate of deposit (CD) and savings account customers can easily qualify for secured personal loans.

Things to Consider Before Consolidation Your Debt

Credit Score

Take a look at your credit score before deciding on how to consolidate your debt. Some consolidation options require a hard credit check, but it’s also important to know that consolidating can help reduce your credit utilization score. This is particularly the case if you make consistent payments over time.

Spending Habits

Before you take out a debt consolidation loan, think about your current personal spending habits and make a plan for how to save more money long term and avoid further debt. Make a firm plan for how to use your consolidation funds to pay off your debt, then put any unused funds towards paying back the new loan. Develop better spending habits by avoiding past negative spending habits and other common financial mistakes.

Debt Consolidation vs Debt Relief

One important distinction to make is between debt consolidation and debt relief. Debt consolidation replaces multiple debts with a single loan, but the same amount still needs to be repaid.

Debt relief or debt settlement reduces debt by negotiating with creditors to let you pay a lower amount. This can have a negative impact on your credit score and future loans may come with higher interest rates. Many debt settlement companies also charge fees around 20-25% of the final settlement cost.

Consolidate Your Debt Today

If you’re looking to consolidate your debt, Citizens Savings Bank can help. Apply now for a personal loan to consolidate your debt, or talk to one of our team to help find the right financial solution for you to help lower your debt in 2024.

Citizens Savings Bank has multiple locations throughout Lackawanna, Wayne, and Monroe Counties. For branch locations and hours, visit our website. We also have a Customer Support Team ready to answer any questions you may have. Call us today at 1.800.692.6279 or email [email protected]. Member FDIC. Equal Housing Lender.